How Private Real Estate Funds Work: A Complete Start to Finish Guide to Structure, Roles, Cash Flow, Reporting and Exits

Private market investing has evolved. Investors today are looking for structured, professionally managed opportunities that offer access to large scale property development without the burden of ownership headaches. Rising interest in alternative assets, income producing strategies, and capital preservation has pushed private real estate funds into the spotlight.

But many investors still ask the same questions:

- How do private real estate funds actually work?

- Who controls the decisions?

- Where does the money go?

- How do investors get paid?

- What happens at exit?

This guide breaks down the complete lifecycle of a private real estate fund from formation to final distribution. You will understand the roles of General Partners and Limited Partners, how cash flows through the structure, what reporting looks like and how investors ultimately realize returns.

If you are exploring equity investment structures, income generating opportunities or long term value creation, this guide will give you clarity.

What Is a Private Real Estate Fund?

A private real estate fund is a pooled investment vehicle that gathers capital from multiple investors to acquire, develop, reposition or finance property projects.

Instead of buying and managing assets individually, investors participate through a professionally structured fund managed by an experienced sponsor.

Private funds are typically structured as:

- Limited Partnerships

- Limited Liability Companies

- Regulation D offerings such as 506B or 506C structures

These funds are not publicly traded. They are offered privately to qualified investors and operate under defined investment strategies and timelines.

The Lifecycle of a Private Real Estate Fund

Understanding the lifecycle helps investors see how capital moves from commitment to distribution.

1. Fund Formation

The process begins with the sponsor or General Partner designing the fund strategy. This includes:

- Defining the investment thesis

- Identifying target asset types

- Establishing risk profile

- Setting return objectives

- Structuring fees and profit splits

- Drafting legal documents

Legal documentation typically includes:

- Private Placement Memorandum

- Limited Partnership Agreement or Operating Agreement

- Subscription Agreement

This documentation outlines how the fund will operate and how investors are protected.

2. Capital Raising Phase

Once structured, the fund begins raising capital from investors.

Investors who commit capital are known as Limited Partners.

During this phase:

- Investors review offering materials

- Due diligence is conducted

- Commitments are signed

- Funds are wired into escrow or operating accounts

Some funds call capital upfront. Others use capital calls as projects are identified.

This phase may last several months depending on the size and scope of the offering.

3. Deployment Phase

After capital is raised, the fund begins acquiring or developing projects according to its strategy.

This could include:

- Ground up development

- Value add repositioning

- Land acquisition

- Structured financing investments

The General Partner manages all execution, including:

- Underwriting

- Financing

- Construction oversight

- Vendor coordination

- Budget management

- Risk mitigation

Limited Partners are passive. They do not participate in day to day operations.

4. Asset Management and Operations

Once projects are active, the focus shifts to performance optimization.

The GP oversees:

- Cost controls

- Schedule adherence

- Strategic decision making

- Market timing

- Performance tracking

This is often the longest stage of the fund lifecycle.

5. Cash Flow Distribution Phase

As projects generate revenue or refinance proceeds, cash distributions may begin.

Depending on the structure, investors may receive:

- Preferred returns

- Profit participation

- Periodic distributions

- Back end profits at sale

Cash flow structure is defined clearly in the operating agreement.

6. Exit Phase

The exit marks the final stage of the fund lifecycle.

Exits typically occur through:

- Asset sale

- Portfolio sale

- Refinance and recapitalization

- Structured buyout

Once assets are sold, profits are distributed according to the waterfall structure.

The fund is then dissolved and investors receive final reporting and distributions.

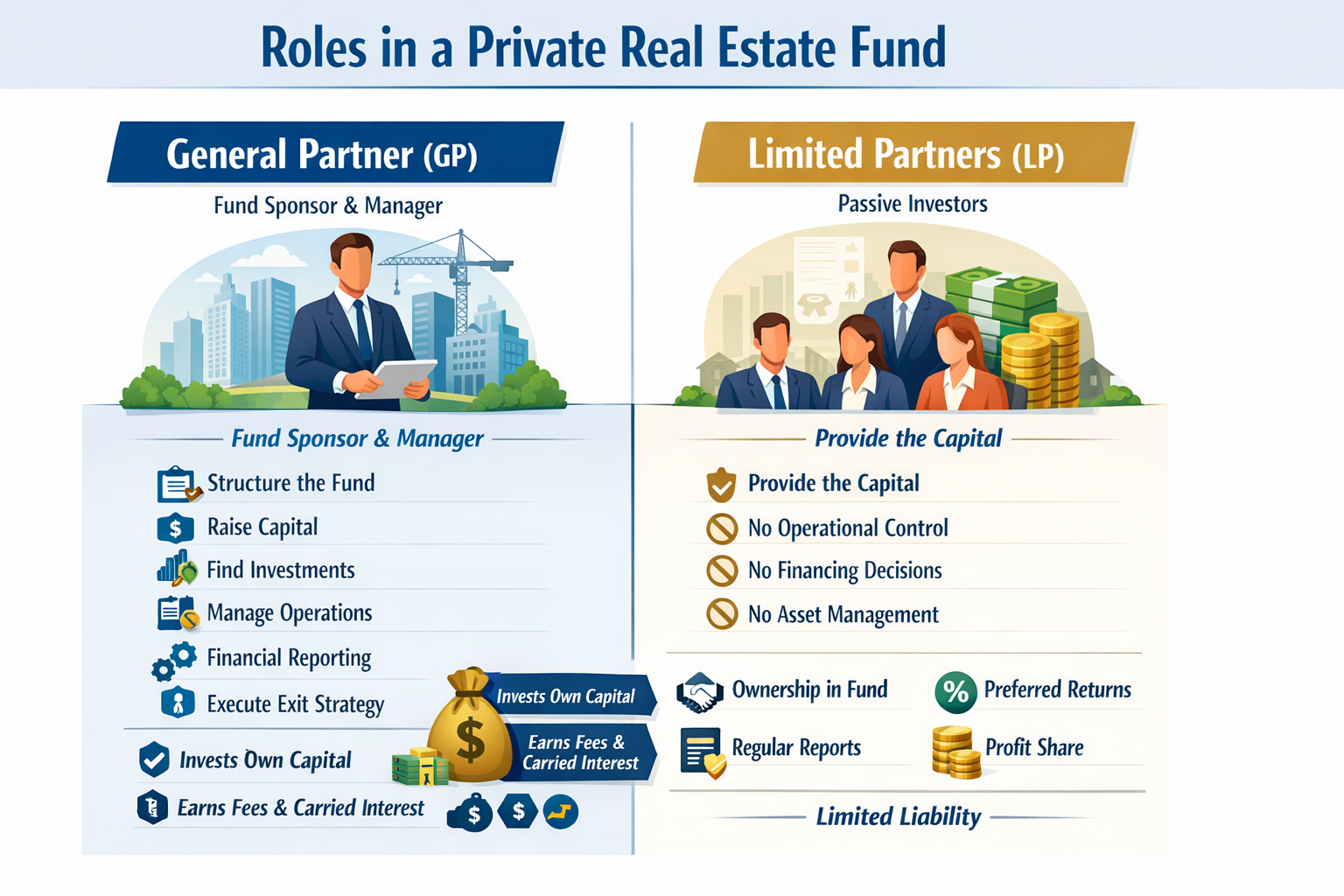

Roles in a Private Real Estate Fund

Understanding the relationship between the General Partner and Limited Partners is critical.

General Partner

The General Partner is the sponsor and manager of the fund.

Responsibilities include:

- Structuring the fund

- Raising capital

- Identifying investment opportunities

- Managing operations

- Overseeing financial reporting

- Executing exit strategy

The GP typically invests their own capital alongside investors to align interests.

Compensation for the GP may include:

- Acquisition fees

- Asset management fees

- Performance based promote or carried interest

The GP carries fiduciary responsibility to act in the best interest of investors.

Limited Partners

Limited Partners provide the capital.

Their role is passive. They do not:

- Make operational decisions

- Sign financing documents

- Manage construction or assets

They receive:

- Ownership interest in the fund

- Defined return structures

- Reporting transparency

- Profit participation

Their liability is limited to their invested capital.

How Cash Flows Work in Private Real Estate Funds

Cash flow is one of the most important components of understanding private funds.

Step 1: Capital Contributions

Investors commit capital. Funds are pooled together and used for:

- Acquisitions

- Development costs

- Financing expenses

- Operating reserves

Step 2: Project Level Income

Once projects begin producing revenue or are sold, cash enters the fund.

Revenue sources may include:

- Sale proceeds

- Refinancing proceeds

- Operating income

- Interest payments in debt funds

Step 3: Distribution Waterfall

Most private funds use a distribution waterfall structure.

A simplified example:

- Return of Capital to Investors

- Preferred Return to Investors

- Catch Up to GP

- Profit Split between LP and GP

This ensures investors are paid first before the GP participates in performance profits.

What Is a Preferred Return?

A preferred return is a targeted annual return that investors receive before the sponsor earns performance compensation.

For example:

If a fund offers an 8 percent preferred return, investors receive that first before profits are split.

Preferred returns are not guaranteed. They depend on performance.

Fee Structures Explained

Private real estate funds generate revenue for sponsors through defined fees.

Common fees include:

- Acquisition Fee

- Asset Management Fee

- Disposition Fee

- Financing Fee

- Promote or Carried Interest

Transparency in fee disclosure is essential. These details are outlined clearly in the Private Placement Memorandum.

Investors should evaluate whether the sponsor has meaningful capital at risk alongside LP investors.

Reporting and Transparency

Strong reporting builds trust and clarity.

Investors typically receive:

- Quarterly performance updates

- Capital account statements

- Project updates

- Financial summaries

- Tax documentation such as Schedule K 1

Good sponsors communicate not just successes but challenges and mitigation strategies.

Reporting may include:

- Project status updates

- Budget tracking

- Timeline progress

- Risk adjustments

- Market outlook

Clear reporting is often a major differentiator between experienced operators and inexperienced sponsors.

Risk Factors Investors Should Understand

Private real estate funds carry risk. No investment is without uncertainty.

Common risks include:

- Market fluctuations

- Construction delays

- Financing risk

- Cost overruns

- Regulatory changes

- Liquidity constraints

Unlike public investments, private fund interests are not easily tradable. Investors should expect capital to remain invested for the duration of the fund term.

Risk mitigation strategies include:

- Conservative underwriting

- Contingency reserves

- Experienced project management

- Diversified project allocation

Timeline Expectations

Private real estate funds are typically long term investments.

Common timelines:

- Development funds may run 3 to 5 years

- Value add strategies may run 3 to 7 years

- Larger portfolios may extend longer

Investors should align their liquidity needs with fund duration.

Why Investors Choose Private Real Estate Funds

Private funds offer benefits that direct ownership does not.

Access to Larger Opportunities

Investors gain exposure to projects that would otherwise require significant capital individually.

Professional Oversight

Experienced sponsors manage every aspect of execution.

Structured Returns

Clear return targets and profit sharing models provide predictability in structure, even though performance can vary.

Passive Participation

Investors avoid operational stress, tenant issues and construction oversight.

Potential for Long Term Value Creation

Strategic development and disciplined execution can create equity growth over time.

How to Evaluate a Private Real Estate Fund

Before investing, consider:

- Sponsor track record

- Alignment of interests

- Transparency of fees

- Risk mitigation strategy

- Reporting structure

- Exit plan clarity

Ask:

- How does the GP get paid?

- What happens if timelines extend?

- What contingencies are in place?

- How often will reporting occur?

Due diligence is critical.

The Exit Strategy Matters More Than the Entry

Sophisticated investors focus heavily on exit.

A strong exit plan includes:

- Defined hold period

- Multiple potential liquidity paths

- Conservative sale assumptions

- Market cycle awareness

Returns are realized at exit. Without a disciplined strategy, projected performance may not materialize.

Tax Considerations

Private real estate funds often provide pass through taxation.

Investors typically receive:

- Schedule K 1 forms

- Allocation of income and losses

- Potential depreciation benefits

Tax outcomes vary based on structure and individual circumstances. Investors should consult qualified advisors.

Common Misconceptions

Misconception 1: Preferred Return Is Guaranteed

It is not guaranteed. It depends on performance.

Misconception 2: Investors Can Withdraw Anytime

Most funds lock capital for the full term.

Misconception 3: All Sponsors Are the Same

Execution quality varies significantly. Experience and discipline matter.

Start to Finish Summary

Here is the lifecycle in simplified order:

- Fund is structured and documented

- Capital is raised from Limited Partners

- Projects are acquired or developed

- Assets are managed and optimized

- Cash flows are distributed per waterfall

- Assets are exited

- Final profits are distributed

- Fund is dissolved

This structured approach allows investors to participate in income generating investments while maintaining a passive role.

Final Thoughts: The Importance of Structure and Sponsor Quality

Private real estate funds are not just about properties. They are about structure, execution and disciplined capital management.

The difference between average performance and exceptional results often comes down to:

- Sponsor experience

- Conservative underwriting

- Transparent communication

- Clear alignment of interests

- Thoughtful exit planning

For investors seeking structured access to professionally managed development strategies, working with a disciplined sponsor matters.

Prawdzik Capitals focuses on creating carefully structured private investment opportunities designed to prioritize transparency, risk awareness and long term value creation. With a defined strategy, aligned incentives and an emphasis on execution, investors gain access to opportunities without operational burdens.

Understanding how private real estate funds work from start to finish empowers you to evaluate opportunities confidently, ask the right questions and position your capital strategically for sustainable growth.

When structure meets execution, private investing becomes a calculated strategy rather than a leap of faith.